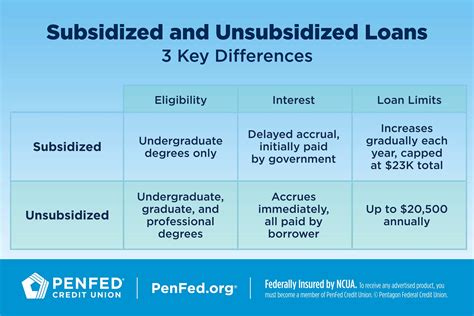

The unsubsidized loan interest rate is a critical factor for borrowers to consider when taking out federal student loans. Unlike subsidized loans, where the government pays the interest while the borrower is in school, unsubsidized loans accrue interest from the moment the loan is disbursed. This means that borrowers are responsible for paying the interest on unsubsidized loans, which can significantly increase the overall cost of the loan over time.

For the 2022-2023 academic year, the interest rate on unsubsidized federal student loans is 4.99% for undergraduate students and 6.54% for graduate and professional students. It's essential to note that these rates are subject to change and are set by Congress each year. Borrowers can expect to pay a fixed interest rate for the life of the loan, unless they consolidate their loans or refinance with a private lender.

Key Points

- The unsubsidized loan interest rate for the 2022-2023 academic year is 4.99% for undergraduate students and 6.54% for graduate and professional students.

- Borrowers are responsible for paying the interest on unsubsidized loans, which can increase the overall cost of the loan over time.

- Interest rates on unsubsidized loans are fixed for the life of the loan, unless the borrower consolidates or refinances with a private lender.

- Unsubsidized loans accrue interest from the moment the loan is disbursed, and borrowers can choose to pay the interest while in school or defer payment until after graduation.

- It's crucial for borrowers to understand the terms and conditions of their unsubsidized loans, including the interest rate, to make informed decisions about their financial aid.

Understanding Unsubsidized Loan Interest Rates

Unsubsidized loan interest rates are determined by the federal government, and the rates are typically announced at the beginning of each academic year. The interest rate is calculated as a percentage of the loan amount and is applied to the outstanding balance. For example, if a borrower takes out a 10,000 unsubsidized loan with an interest rate of 4.99%, they can expect to pay approximately 499 in interest over the life of the loan, assuming a 10-year repayment period.

It's essential to note that unsubsidized loans have a higher interest rate than subsidized loans, which can make them more expensive for borrowers in the long run. However, unsubsidized loans are still a popular option for many students, as they offer more flexible repayment terms and do not require borrowers to demonstrate financial need.

Types of Unsubsidized Loans

There are several types of unsubsidized loans available to students, including:

- DIRECT UNSUBSIDIZED LOANS: These loans are available to undergraduate and graduate students and do not require borrowers to demonstrate financial need.

- GRADUATE PLUS LOANS: These loans are available to graduate and professional students and have a higher interest rate than DIRECT UNSUBSIDIZED LOANS.

- PARENT PLUS LOANS: These loans are available to parents of dependent undergraduate students and have a higher interest rate than DIRECT UNSUBSIDIZED LOANS.

Each type of unsubsidized loan has its own set of terms and conditions, including the interest rate, fees, and repayment terms. Borrowers should carefully review the terms of their loan before accepting the funds.

| Loan Type | Interest Rate | Fees |

|---|---|---|

| DIRECT UNSUBSIDIZED LOANS | 4.99% (undergraduate), 6.54% (graduate) | 1.057% (origination fee) |

| GRADUATE PLUS LOANS | 7.54% | 4.236% (origination fee) |

| PARENT PLUS LOANS | 7.54% | 4.236% (origination fee) |

Strategies for Managing Unsubsidized Loan Interest

While unsubsidized loans can be more expensive than subsidized loans, there are several strategies that borrowers can use to manage their interest and reduce the overall cost of their loan. Some of these strategies include:

- Paying the interest while in school: By paying the interest on their unsubsidized loan while they are still in school, borrowers can avoid capitalization and reduce the overall cost of their loan.

- Consolidating loans: Borrowers who have multiple unsubsidized loans with different interest rates may be able to consolidate their loans into a single loan with a lower interest rate.

- Refinancing with a private lender: Borrowers who have a good credit score may be able to refinance their unsubsidized loan with a private lender at a lower interest rate.

It's essential to note that each of these strategies has its own set of pros and cons, and borrowers should carefully consider their options before making a decision.

What is the current interest rate on unsubsidized federal student loans?

+The current interest rate on unsubsidized federal student loans is 4.99% for undergraduate students and 6.54% for graduate and professional students.

How do unsubsidized loan interest rates affect the overall cost of the loan?

+Unsubsidized loan interest rates can significantly increase the overall cost of the loan over time. Borrowers are responsible for paying the interest on unsubsidized loans, which can add up quickly.

What strategies can borrowers use to manage their unsubsidized loan interest?

+Borrowers can use several strategies to manage their unsubsidized loan interest, including paying the interest while in school, consolidating loans, and refinancing with a private lender.