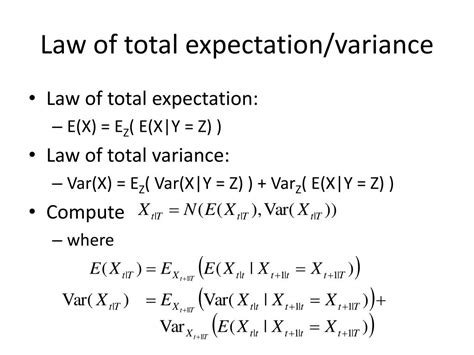

The Law of Total Expectation, also known as the Law of Iterated Expectations, is a fundamental concept in probability theory and statistics. It states that the expected value of a random variable can be calculated by conditioning on another random variable, and then taking the expected value of the resulting expression. This law is crucial in a wide range of applications, including finance, engineering, and economics, as it allows for the simplification of complex calculations and the analysis of conditional probabilities.

In essence, the Law of Total Expectation provides a powerful tool for breaking down complex problems into more manageable components. By conditioning on a specific event or random variable, researchers and analysts can gain insight into the relationships between different variables and how they contribute to the overall expected value. This is particularly useful in situations where the joint distribution of multiple random variables is difficult to model or analyze directly.

Key Points

- The Law of Total Expectation is used to calculate the expected value of a random variable by conditioning on another random variable.

- It is a fundamental concept in probability theory and statistics, with applications in finance, engineering, and economics.

- The law allows for the simplification of complex calculations and the analysis of conditional probabilities.

- It provides a powerful tool for breaking down complex problems into more manageable components.

- The Law of Total Expectation is essential in situations where the joint distribution of multiple random variables is difficult to model or analyze directly.

Mathematical Formulation

The Law of Total Expectation can be mathematically formulated as follows: Let X and Y be two random variables, and suppose that the conditional expectation of X given Y is known. Then, the expected value of X can be calculated as the expected value of the conditional expectation of X given Y. This can be expressed as:

E(X) = E(E(X|Y))

This equation states that the expected value of X is equal to the expected value of the conditional expectation of X given Y. The conditional expectation E(X|Y) is a random variable that depends on the value of Y, and the outer expectation E() is taken with respect to the distribution of Y.

Conditional Expectation

The conditional expectation E(X|Y) is a fundamental concept in the Law of Total Expectation. It represents the expected value of X given that Y has taken on a specific value. The conditional expectation is a random variable that depends on the value of Y, and it is defined as the expected value of X given that Y = y, where y is a specific value of Y.

The conditional expectation can be calculated using the formula:

E(X|Y=y) = ∫xf(x|y)dx

where f(x|y) is the conditional probability density function of X given Y = y. The conditional probability density function is a function of x and y, and it represents the probability density of X given that Y = y.

| Random Variable | Conditional Expectation |

|---|---|

| X | E(X|Y=y) = ∫xf(x|y)dx |

| Y | E(Y|X=x) = ∫yf(y|x)dy |

Applications

The Law of Total Expectation has a wide range of applications in finance, engineering, and economics. In finance, it is used to calculate the expected return on investment, to price options and other derivatives, and to manage risk. In engineering, it is used to analyze complex systems, to optimize performance, and to predict future outcomes. In economics, it is used to model economic systems, to analyze the impact of policy interventions, and to predict future economic trends.

One of the key applications of the Law of Total Expectation is in the field of risk analysis. By conditioning on specific events or random variables, researchers and analysts can gain insight into the potential risks and rewards associated with different courses of action. This can be used to inform decision-making, to optimize performance, and to minimize risk.

Risk Analysis

Risk analysis is a critical component of decision-making in a wide range of fields, including finance, engineering, and economics. The Law of Total Expectation provides a powerful tool for analyzing risk, by allowing researchers and analysts to condition on specific events or random variables and to calculate the expected value of different outcomes.

The Law of Total Expectation can be used to analyze risk in a variety of ways, including:

1. Calculating the expected value of different outcomes, given specific events or random variables.

2. Analyzing the sensitivity of different outcomes to changes in underlying variables.

3. Identifying potential risks and rewards associated with different courses of action.

What is the Law of Total Expectation?

+The Law of Total Expectation is a fundamental concept in probability theory and statistics, which states that the expected value of a random variable can be calculated by conditioning on another random variable, and then taking the expected value of the resulting expression.

How is the Law of Total Expectation used in finance?

+The Law of Total Expectation is used in finance to calculate the expected return on investment, to price options and other derivatives, and to manage risk.

What is the conditional expectation?

+The conditional expectation is a random variable that depends on the value of another random variable, and it represents the expected value of a random variable given that another random variable has taken on a specific value.

In conclusion, the Law of Total Expectation is a powerful tool for analyzing complex systems and making predictions about future outcomes. By conditioning on specific events or random variables, researchers and analysts can gain insight into the relationships between different variables and how they contribute to the overall expected value. The Law of Total Expectation has a wide range of applications in finance, engineering, and economics, and it is essential for anyone working in these fields to have a deep understanding of this concept.